THE OVERTHROW OFWEIGHTS AND MEASURES IS CHAOS WEAPONIZED.

1. Bring and restore all mining under the People’s Treasury.

2. Bring all Human Energy (Labor) under the people’s Treasury.

3. Then issue overnight currency supply ballasted on current production, in accordance to the ancient law and root value of “Weights AND Measures.”

4. MINING, ballasted in Bonds, future production.

5. TAX-EXEMPTED CENTRAL BANKING SCHEME IS IMITATION CAPITALISM.

6.2022.7.26. RUSSIA/CHINA HEAD IN THIS DIRECTION!

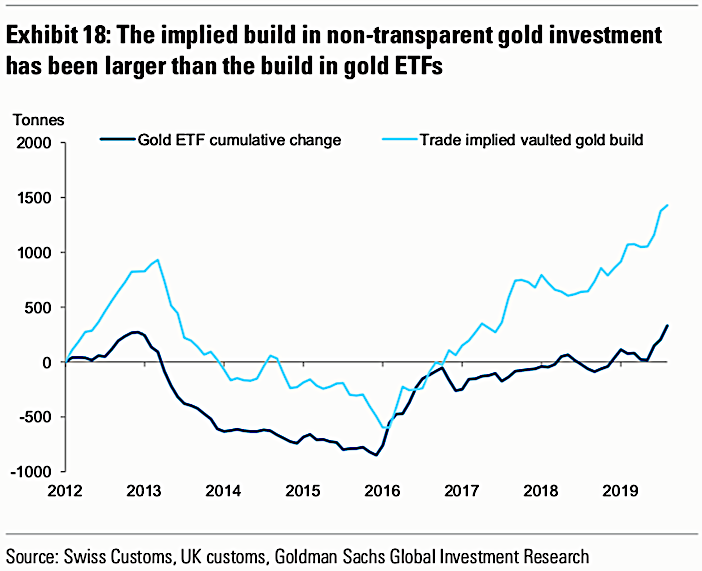

The world’s rich are hoarding gold – this according to data buried in a recent Goldman Sachs note to clients.

In the note published over the weekend, Goldman recommended diversifying long-term bond holdings with gold, citing “fear-driven demand” for the yellow metal.

Hedge funds and other large speculators boosted their bullish bets on gold by 8.9% through the week ended Dec. 3, according to government data released last Friday. That represents the biggest gain since the end of September.

The Goldman note cited political uncertainty and recession fears as the catalyst for the move toward gold. It also mentioned worries about a wealth tax, increasing interest in Modern Monetary Theory (essentially money-printing) and the current loose central bank monetary policy.

Data buried in the note also revealed that owning physical gold appears to be the preferred method to “hedge against tail events” by the rich.

"Since the end of 2016 the implied build in non-transparent gold investment has been much larger than the build in visible gold ETFs.”

Goldman said the data is consistent with reports that vault demand is surging globally.

Trade data implies that gold in storage has increased far more rapidly than is reflected by financial market instruments, indicating a widespread preference for physical gold instead of gold-linked financial assets … Political risks, in our view, help explain this because if an individual is trying to minimize the risks of sanctions or wealth taxes, then buying physical gold bars and storing them in a vault, where it is more difficult for governments to reach them, makes sense.

“Finally, this build can also reflect hedges by global high net worth individuals against tail economic and political risk scenarios in which they do not want to have any financial entity intermediating their gold positions due to the counter-party credit risk involved.”

As a writer for Yahoo Finance put it.

“This means that for those including gold in their end-of-the-world trade, owning gold bullion is a must.”

You don’t have to be super-rich to invest in gold. And the same reasons the wealthy are hoarding the yellow metal apply to average investors. In a world drowning in government, corporate and consumer debt, and with never-ending loose monetary policy, along with and a political landscape becoming more and more favorable to socialism, it makes sense to own physical gold and store it securely so you have access to your wealth with minimal counterparty risk.

THERE IS NO WAY ANY ECONOMY CAN HAVE IT BOTH WAYS, IE, JOBS-MANUFACTURING + FINANCIAL INSTITUTION.

TRANSLATION: A GLOBAL CURRENCY (GNP) IS TOO EXPENSIVE AND OVERVALUED FOR DOMESTIC GDP MANUFACTURING AND SUBSEQUENT JOBS.

SOLUTION: CRASH THE FEDERAL RESERVE CENTRAL BANK-GOVT.'S FREE PAPER CURRENCY WITH NEGATIVE BENCHMARK RATES AND TARIFF HIKES ON IMPORTS, WHICH WILL IN TURN RECOVER LOST US JOBS-MANUFACTURING AFTER 1970.

OVER 200-COUNTRIES WILL LOOSE IN THEIR EXPORTS TO THE US.

IN THE END ALL WILL BENEFIT AS "WEIGHTS & MEASURES" IS CONSTITUTIONALLY RESTORED AND PEGGED TO BULLION AND CRYPTOS.

The number of Americans filing applications for unemployment benefits fell to more than a 49-year low last week, but the drop ...

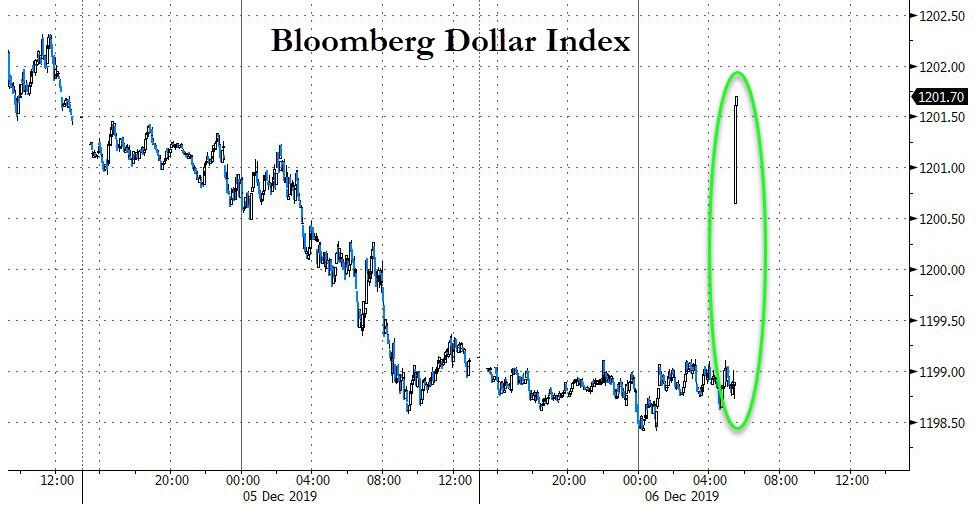

Stocks, Dollar, & Bond Yields Surge After Huge Jobs Beat

Following a much better than expected jobs gain in November, markets have reacted rather dramatically with bond yields and the dollar gapping higher and stocks jumping...

The dollar erased yesterday's drop...

Source: Bloomberg

And 30Y Yields are spiking back to the highs on Monday...

Source: Bloomberg

And as the dollar spikes, gold is hit...

Kudlow is due up next on CNBC so that should help too...

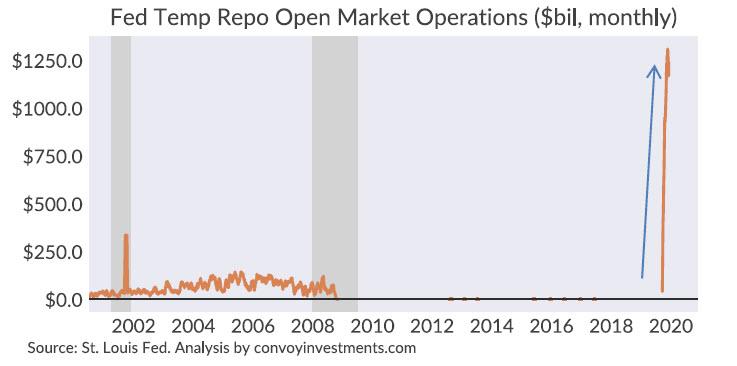

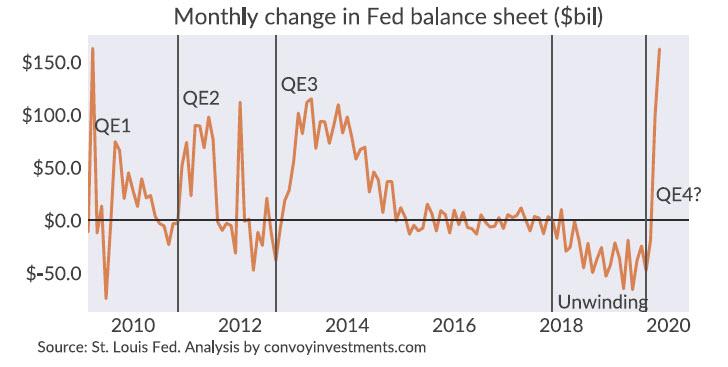

"The Fed Hasn't Expanded Its Balance Sheet At This Speed Since The Financial Crisis"

Has QE4 begun? The $1.2 trillion per month hole in the repo market.

In the two months since the repo market blow up, the Fed has been making repo open market operation purchases at a rate of $1.2 trillion per month.

Below is the monthly rate of Fed open market purchases since 2000. In the era of QE and ample reserves, the Fed has not touched open market operations for more than 10 years before 2019. Prior to that, the highest rate of open market operations we saw in history was roughly $300 billion/month briefly after the September 11 attacks, with long‐term averages of around $50 billion/month. To say the current rate of $1.2 trillion/month is unprecedented would be an understatement

The planned QE unwinding has hit a brick wall and the Fed balance sheet is now expanding at a rate matched only briefly by QE1, and faster than QE2 or QE3.

Is this a temporary rescue of the repo market or the start of a sustained QE4? To answer that question, we must look at how monetary policy has evolved since the Financial Crisis.

1. Pre‐2008, scarce reserves regime:

Total reserves: small (<$50 billion)

Excess reserves: none

Interest on excess reserves: 0%

Managing interest rates: to increase rates, Fed sells securities on the open market and reduces supply of reserves, vice versa to decrease rates.

Banks: regulations are lax and risk tolerance is high

Treasury department: carefully manages its cash flows to not impact the total reserve levels.

2. 2008‐2019, ample reserves regime:

Total reserves: large ($trillions)

Excess reserves: large ($trillions)

Interest on excess reserves: positive at around Fed funds rate

Managing interest rates: Because there is more reserves than the banks could possibly need, Fed sets interest rates by paying a floor rate on reserves.

Banks: regulations are strict and risk tolerance is low

Treasury department: no longer actively manages its cash flows, its activities directly affect total reserve levels.

3. 2019 onwards, scarce reserves regime again?:

A combination of QE unwinding, strict banking regulations, and a concentration of reserves in a handful of banks have once again made reserves scarce, which means a rate floor is no longer effective at managing against rate rises. This was painfully obvious in December of 2018 and September of 2019. Thus far, the Fed has chosen their pre‐2008 strategy of temporary open market operations to manage rates in this new scarce reserves environment. But because the total pool of reserves is around 50 times larger now than pre‐2008, the size of the required open market operations is in the $trillions, not $billions, per month.

Going forward, the Fed must make a choice of staying in a regime of scarce reserves or going back to ample reserves. The Fed can lower interest on excess reserves and reduce bank incentives to hold excess reserves to some degree, but the new post‐2008 regulations will still necessitate a far larger base of reserves than pre‐2008. So managing a scarce reserves banking system on a large base of reserves will require continued massive open market operations. It will likely also require a change from the Treasury department’s cash flow management.

Alternatively, the Fed can recognize that they’ve found the floor for the total amount of reserves necessary in our new regulatory environment and add some reserves via another round of QE as cushion and grow the total reserves in line with our GDP. This would allow us to stay in the ample reserves regime.

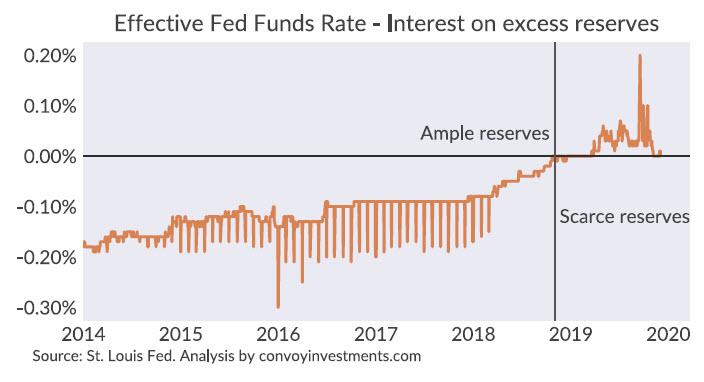

The key metric I’d keep an eye on is the difference between interest on excess reserves and the effective Fed Funds rate, which I show below. We made the switch from an ample reserves regime to a scarce reserves regime in December of 2018.

If the system has more than enough reserves, the effective Fed Funds rate would be below the interest on excess reserves because not every participant is eligible for interest on excess reserves, hence they’d push the average Fed Funds rate below interest on excess reserves. In the 2019 environment of scarce reserves, market participants are starved for reserves and bid the average Fed Funds rate at or above interest on excess reserves. At the moment, the Fed has done enough open market operations to meet reserve demand and drive Fed Funds rate exactly back to interest on excess reserves.

Going forward, whether the Fed pushes effective Fed Funds rate below interest on excess reserves will signal the next era of monetary policy. If the Fed chooses the scarce reserves route, Fed funds rate will stay at or above interest on excess reserves. The Fed will continue to buy short‐term securities as necessary to meet demand for reserves and push down the short end of the curve and I’d bet on the yield curve steepening again. If they choose the ample reserves route, Fed Funds rate will fall back below interest on excess reserves, the Fed will go back to buying 10 year bonds, and I’d expect to see further flattening of the yield curve.

Unless banking regulations change dramatically, my guess is that QE4 is coming. The Fed would rather have a cushion of ample reserves against unexpected repo market blow ups than react retroactively with $trillions/month of open market operation purchases.