<a data-pin-do="embedBoard " href="https://br.pinterest.com/carsbikesandroc/annunaki-ponnzi-currencies-exchanged-for-fort-knox/"data-pin-scale-width="80" data-pin-scale-height="200" data-pin-board-width="400"> Siga a pasta ANNUNAKI PONNZI CURRENCIES EXCHANGED FOR FORT KNOX GOLD? de Tag no Pinterest .</a><!-- Please call pinit.js only once per page --><script type="text/javascript" async src="//assets.pinterest.com/js/pinit.js"></script>

The first global Ponzi collapse is impossible, yet the impossible is also a possibility.

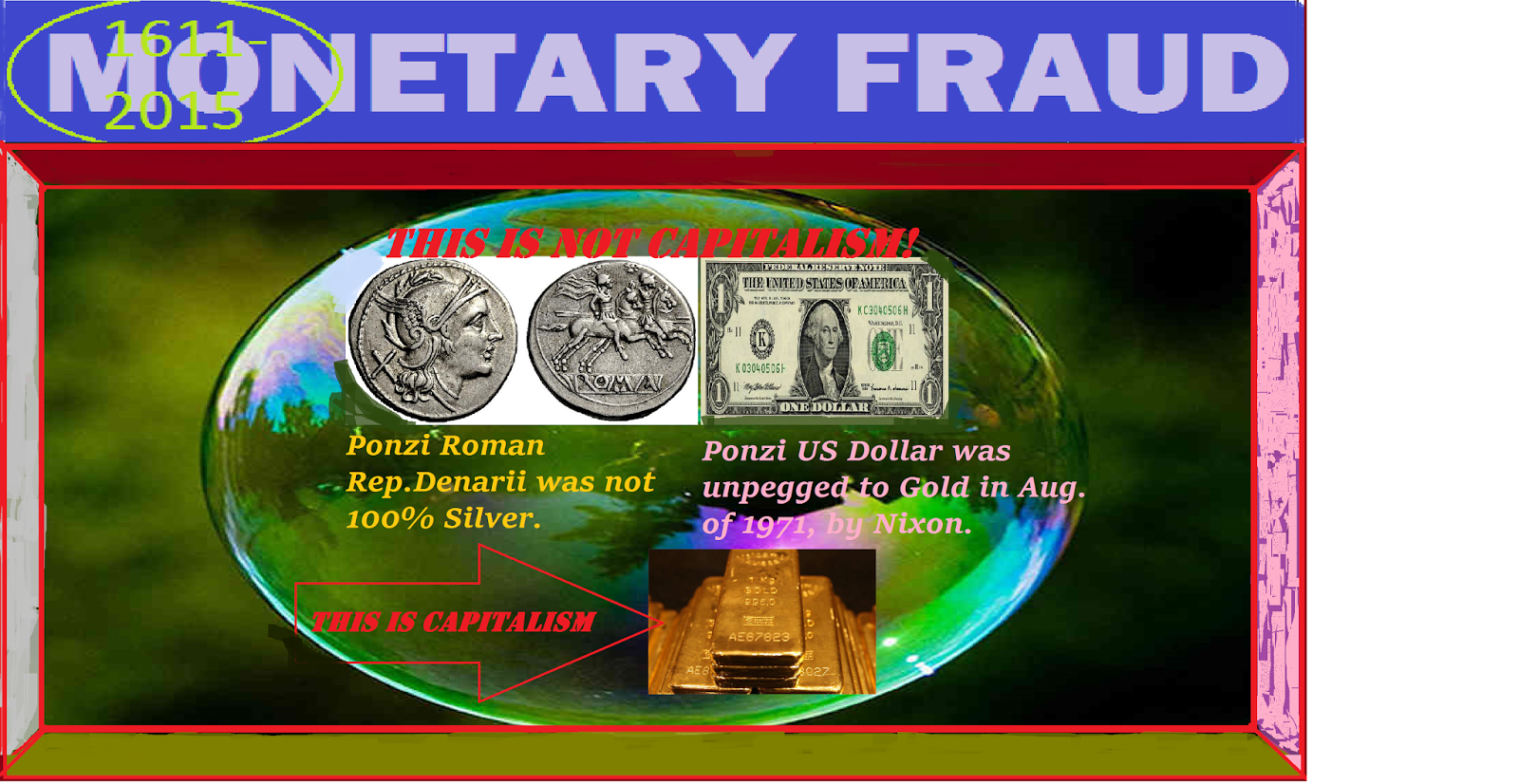

Similarly, the Roman Empire operated under a supposedly hard currency scheme and quietly turned out into Ponzi silver. Since August of l971, Nixon quietly turned the USDollar into a Ponzi paper currency hereabouts. ===================================+++++++++++++++++++++++++++++++++++++++++++++

August, 1971, Nixon destroys the US Dollar by unpeggingit from gold since Bretton Woods treaty (later IMF) in 1945. Then says that he is defending the Dollar.

https://www.imf.org/external/about/histend.htm

+++++++++++++++++++++++++++++++++++++++++++++++++++++++

At its peak, the Roman Empire held up to 130 million people over a span of 1.5 million square miles.

Rome had conquered much of the known world. The Empire built 50,000 miles of roads, as well as many aqueducts, amphitheatres, and other works that are still in use today.

Our alphabet, calendar, languages, literature, and architecture borrow much from the Romans. Even concepts of Roman justice still stand tall, such as being “innocent until proven guilty”.

So, as Visual Capitalist's Jeff Desjardins' asks, how could such a powerful empire collapse?

The Roman Economy

Trade was vital to Rome. It was trade that allowed a wide variety of goods to be imported into its borders: beef, grains, glassware, iron, lead, leather, marble, olive oil, perfumes, purple dye, silk, silver, spices, timber, tin and wine.

Trade generated vast wealth for the citizens of Rome. However, the city of Rome itself had only 1 million people, and costs kept rising as the empire became larger.

Administrative, logistical, and military costs kept adding up, and the Empire found creative new ways to pay for things.

Along with other factors, this led to hyperinflation , a fractured economy, localization of trade, heavy taxes, and a financial crisis that crippled Rome.

Roman Debasement

The major silver coin used during the first 220 years of the empire was the denarius .

This coin, between the size of a modern nickel and dime, was worth approximately a day’s wages for a skilled laborer or craftsman. During the first days of the Empire, these coins were of high purity, holding about 4.5 grams of pure silver.

However, with a finite supply of silver and gold entering the empire, Roman spending was limited by the amount of denarii that could be minted.

This made financing the pet-projects of emperors challenging. How was the newest war, thermae , palace, or circus to be paid for?

Roman officials found a way to work around this. By decreasing the purity of their coinage, they were able to make more “silver” coins with the same face value. With more coins in circulation, the government could spend more. And so, the content of silver dropped over the years.

By the time of Marcus Aurelius, the denarius was only about 75% silver. Caracalla tried a different method of debasement. He introduced the “double denarius ”, which was worth 2x the denarius in face value. However, it had only the weight of 1.5 denarii . By the time of Gallienus, the coins had barely 5% silver. Each coin was a bronze core with a thin coating of silver. The shine quickly wore off to reveal the poor quality underneath.

The Consequences

The real effects of debasement took time to materialize.

Adding more coins of poorer quality into circulation did not help increase prosperity – it just transferred wealth away from the people, and it meant that more coins were needed to pay for goods and services.

At times, there was runaway inflation in the empire. For example, soldiers demanded far higher wages as the quality of coins diminished.

“Nobody should have any money but I, so that I may bestow it upon the soldiers.” – Caracalla, who raised soldiers pay by 50% near 210 AD.

By 265 AD, when there was only 0.5% silver left in a denarius , prices skyrocketed 1,000% across the Roman Empire.

Only barbarian mercenaries were to be paid in gold.

Only barbarian mercenaries were to be paid in gold.

The Effects

With soaring logistical and admin costs and no precious metals left to plunder from enemies, the Romans levied more and more taxes against the people to sustain the Empire.

The economy was paralyzed.

By the end of the 3rd century, any trade that was left was mostly local, using inefficient barter methods instead of any meaningful medium of exchange.

The Collapse

During the crisis of the 3rd century (235-284 A.D), there may have been more than 50 emperors. Most of these were murdered, assassinated, or killed in battle.

The empire was in a free-for-all, and it split into three separate states.

Constant civil wars meant the Empire’s borders were vulnerable. Trade networks were disintegrated and such activities became too dangerous.

Barbarian invasions came in from every direction. Plague was rampant.

And so the Western Roman Empire would cease to exist by 476 A.D.

++++++++++++++++++++++++++++++++++++++++++++++++++

The US economy died when middle class jobs were offshored and when the financial system was deregulated.

Jobs offshoring benefitted Wall Street, corporate executives, and shareholders, because lower labor and compliance costs resulted in higher profits. These profits flowed through to shareholders in the form of capital gains and to executives in the form of “performance bonuses.” Wall Street benefitted from the bull market generated by higher profits.

However, jobs offshoring also offshored US GDP and consumer purchasing power. Despite promises of a “New Economy” and better jobs, the replacement jobs have been increasingly part-time, lowly-paid jobs in domestic services, such as retail clerks, waitresses and bartenders.

The offshoring of US manufacturing and professional service jobs to Asia stopped the growth of consumer demand in the US, decimated the middle class, and left insufficient employment for college graduates to be able to service their student loans. The ladders of upward mobility that had made the United States an “opportunity society” were taken down in the interest of higher short-term profits.

Without growth in consumer incomes to drive the economy, the Federal Reserve under Alan Greenspan substituted the growth in consumer debt to take the place of the missing growth in consumer income. Under the Greenspan regime, Americans’ stagnant and declining incomes were augmented with the ability to spend on credit. One source of this credit was the rise in housing prices that the Federal Reserves low inerest rate policy made possible. Consumers could refinance their now higher-valued home at lower interest rates and take out the “equity” and spend it.

The debt expansion, tied heavily to housing mortgages, came to a halt when the fraud perpetrated by a deregulated financial system crashed the real estate and stock markets. The bailout of the guilty imposed further costs on the very people that the guilty had victimized.

Under Fed chairman Bernanke the economy was kept going with Quantitative Easing, a massive increase in the money supply in order to bail out the “banks too big to fail.” Liquidity supplied by the Federal Reserve found its way into stock and bond prices and made those invested in these financial instruments richer. Corporate executives helped to boost the stock market by using the companies’ profits and by taking out loans in order to buy back the companies’ stocks, thus further expanding debt.

Those few benefitting from inflated financial asset prices produced by Quantitative Easing and buy-backs are a much smaller percentage of the population than was affected by the Greenspan consumer credit expansion. A relatively few rich people are an insufficient number to drive the economy.

The Federal Reserve’s zero interest rate policy was designed to support the balance sheets of the mega-banks and denied Americans interest income on their savings. This policy decreased the incomes of retirees and forced the elderly to reduce their consumption and/or draw down their savings more rapidly, leaving no safety net for heirs.

Using the smoke and mirrors of under-reported inflation and unemployment, the US government kept alive the appearance of economic recovery. Foreigners fooled by the deception continue to support the US dollar by holding US financial instruments.

The official inflation measures were “reformed” during the Clinton era in order to dramatically understate inflation. The measures do this in two ways. One way is to discard from the weighted basket of goods that comprises the inflation index those goods whose price rises. In their place, inferior lower-priced goods are substituted.

For example, if the price of New York strip steak rises, round steak is substituted in its place. The former official inflation index measured the cost of a constant standard of living. The “reformed” index measures the cost of a falling standard of living.

The other way the “reformed” measure of inflation understates the cost of living is to discard price rises as “quality improvements.” It is true that quality improvements can result in higher prices. However, it is still a price rise for the consumer as the former product is no longer available. Moreover, not all price rises are quality improvements; yet many prices rises that are not can be misinterpreted as “quality improvements.”

These two “reforms” resulted in no reported inflation and a halt to cost-of-living adjustments for Social Security recipients. The fall in Social Security real incomes also negatively impacted aggregate consumer demand.

The rigged understatement of inflation deceived people into believing that the US economy was in recovery. The lower the measure of inflation, the higher is real GDP when nominal GDP is deflated by the inflation measure. By understating inflation, the US government has overstated GDP growth.

What I have written is easily ascertained and proven; yet the financial press does not question the propaganda that sustains the psychology that the US economy is sound. This carefully cultivated psychology keeps the rest of the world invested in dollars, thus sustaining the House of Cards.

John Maynard Keynes understood that the Great Depression was the product of an insufficiency of consumer demand to take off the shelves the goods produced by industry. The post-WW II macroeconomic policy focused on maintaining the adequacy of aggregate demand in order to avoid high unemployment. The supply-side policy of President Reagan successfully corrected a defect in Keynesian macroeconomic policy and kept the US economy functioning without the “stagflation” from worsening “Philips Curve” trade-offs between inflation and employent . In the 21st century, jobs offshoring has depleted consumer demand’s ability to maintain US full employment.

The unemployment measure that the presstitute press reports is meaningless as it counts no discouraged workers, and discouraged workers are a huge part of American unemployment. The reported unemployment rate is about 5%, which is the U-3 measure that does not count as unemployed workers who are too discouraged to continue searching for jobs.

The US government has a second official unemployment measure, U-6, that counts workers discouraged for less than one-year. This official rate of unemployment is 10%.

When long term (more than one year) discouraged workers are included in the measure of unemployment, as once was done, the US unemployment rate is 23%. (See John Williams, shadowstats.com)

Fiscal and monetary stimulus can pull the unemployed back to work if jobs for them still exist domestically. But if the jobs have been sent offshore, monetary and fiscal policy cannot work.

What jobs offshoring does is to give away US GDP to the countries to which US corporations move the jobs. In other words, with the jobs go American careers, consumer purchasing power and the tax base of state, local, and federal governments. There are only a few American winners, and they are the shareholders of the companies that offshored the jobs and the executives of the companies who receive multi-million dollar “performance bonuses” for raising profits by lowering labor costs. And, of course, the economists, who get grants, speaking engagements, and corporate board memberships for shilling for the offshoring policy that worsens the distribution of income and wealth. An economy run for a few only benefits the few, and the few, no matter how large their incomes, cannot consume enough to keep the economy growing.

In the 21st century US economic policy has destroyed the ability of real aggregate demand in the US to increase. Economists will deny this, because they are shills for globalism and jobs offshoring. They misrepresent jobs offshoring as free trade and, as in their ideology free trade benefits everyone, claim that America is benefitting from jobs offshoring. Yet, they cannot show any evidence whatsoever of these alleged benefits. (See my book, The Failure of Laissez Faire Capitalism and Economic Dissolution of the West.)

As an economist, it is a mystery to me how any economist can think that a population that does not produce the larger part of the goods that it consumes can afford to purchase the goods that it consumes. Where does the income come from to pay for imports when imports are swollen by the products of offshored production?

We were told that the income would come from better-paid replacement jobs provided by the “New Economy,” but neither the payroll jobs reports nor the US Labor Departments’s projections of future jobs show any sign of this mythical “New Economy.”

There is no “New Economy.” The “New Economy” is like the neoconservatives promise that the Iraq war would be a six-week “cake walk” paid for by Iraqi oil revenues, not a $3 trillion dollar expense to American taxpayers (according to Joseph Stiglitz and Linda Bilmes) and a war that has lasted the entirety of the 21st century to date, and is getting more dangerous.

The American “New Economy” is the American Third World economy in which the only jobs created are low productivity, low paid nontradable domestic service jobs incapable of producing export earnings with which to pay for the goods and services produced offshore for US consumption.

The massive debt arising from Washington’s endless wars for neoconservative hegemony now threaten Social Security and the entirety of the social safety net. The presstitute media are blaming not the policy that has devasted Americans, but, instead, the Americans who have been devasted by the policy.

Earlier this month I posted readers’ reports on the dismal job situation in Ohio, Southern Illinois, and Texas. In the March issue of Chronicles, Wayne Allensworth describes America’s declining rural towns and once great industrial cities as consequences of “globalizing capitalism.” A thin layer of very rich people rule over those “who have been left behind”—a shrinking middle class and a growing underclass. According to a poll last autumn, 53 percent of Americans say that they feel like a stranger in their own country.

Most certainly these Americans have no political representation. As Republicans and Democrats work to raise the retirement age in order to reduce Social Security outlays, Princeton University experts report that the mortality rates for the white working class are rising. The US government will not be happy until no one lives long enough to collect Social Security.

The United States government has abandoned everyone except the rich.

In the opening sentence of this article, I said that the two murderers of the American economy were jobs offshoring and financial deregulation. Deregulation greatly enhanced the ability of the large banks to financialize the economy. Financialization is the diversion of income streams into debt service. When debt service absorbs a large amount of the available income, the economy experiences debt deflation. The service of debt leaves too little income for purchases of goods and services and prices fall.

Michael Hudson, who I recently wrote about, is the expert on finanialization . His book, Killing the Host, which I recommended to you, tells the complete story. Briefly, financialization is the process by which creditors capitalize an economy’s economic surplus into interest payments to themselves. Perhaps an example would be a corporation that goes into debt in order to buy back its shares. The corporation achieves a temporary boost in its share prices at the cost of years of interest payments that drain the corporation of profits and deflate its share price.

Michael Hudson stresses the conversion of the rental value of real estate into mortgage payments. He emphasizes that classical economists wanted to base taxation not on production, but on economic rent. Economic rent is value due to location or to a monopoly position. For example, beachfront property has a higher price because of location. The difference in value between beachfront and nonbeachfront property is economic rent, not a produced value. An unregulated monopoly can charge a price for a service that is higher than the price that would bring that service unto the market.

The proposal to tax economic rent does not mean taxing you on the rent that you pay your landlord or taxing your landlord on the rent that you pay him such that he ceases to provide the housing. By economic rent Hudson means, for example, the rise in land values due to public infrastructure projects such as roads and subway systems. The rise in the value of land opened by a new road and in housing and commercial space along a new subway line is not due to any action of the property owners. This rise in value could be taxed in order to pay for the project instead of taxing the income of the population in general. Instead, the rise in land values raises appraisals and the amount that creditors are willing to lend on the property. New purchasers and existing owners can borrow more on the property, and the larger mortgages divert the increased land valuation into interest payments to creditors. Lenders end up as the major beneficiaries of public projects that raise real estate prices.

Similarly, unless the economy is financialized to such an extent that mortgage debt can no longer be serviced, when central banks lower interest rates property values rise, and this rise can be capitalized into a larger mortgage.

Another example would be property tax reductions and legislation such as California’s Proposition 13 that freeze in whole or part the property tax base. The rise in real estate values that escape taxation are capitalized into larger mortgages. New buyers do not benefit. The beneficiaries are the lenders who capture the rise in real estate prices in interest payments.

Taxing economic rent would prevent the financial system from capitalizing the rent into debt instruments that pay interest to the financial sector. Considering the amount of rents available to be taxed, taxing rents would free production from income and sales taxation, thus lowering consumer prices and freeing labor and productive capital from taxation.

With so much of land rent already capitalized into debt instruments shifting the tax burden to economic rent would be challenging. Nevertheless, Hudson’s analysis shows that financialization , not wage suppression, is the main instrument of exploitation and takes place via the financial system’s conversion of income streams into interest payments on debt.

I remember when mortgage service was restricted to one-quarter of household income. Today mortgage service can eat up half of household income. This extraordinary growth crowds out the production of goods and services as less of household income is available for other purchases.

Michael Hudson and I bring a total indictment of the neoliberal economics profession, “junk economists” as Hudson calls them.

No comments:

Post a Comment